Money

How To Get Paid to Read Books? (9 Best & Legit Sites)

Did you know that your hobby of reading books could get you soo much money?

There are many opportunities out there that will pay you for reading and reviewing the books. This is not only the easiest way to earn some gigs but also to get free books and get your name out there. You can read those books from the comfort of your homes and your flexibility. You can choose the genre of your interest from many categories like fiction, non-fiction, crime novels, self-help manuscripts, and motivational books.

To assist you in earning money while you read books, this article has bought forth a list of websites that get you paid for reading.

How much book readers are paid?

Honestly, the amount you get paid depends on the number of books you read. It is a great advantage of you are a fast reader. You could finish 1 2 books each day and earn more than an average person. You can earn up to $20 per hour. However, this varies according to the website you read for, and the time spend on reading.

How They Pay You:

Yes, there are many popular websites that will pay you for reviewing books. Payment methods often include cash through PayPal or bank transfers, and in some cases, you may also receive a complimentary book in exchange for your review.

10 Websites That Pay You to Read Books:

Here are the 10 Websites that pay you to read books. We have chosen the best websites available and that are willing to pay the best price for your time.

1. Kirkus Reviews:

Kirkus Reviews is a platform that specializes in reviewing books. They have a large number of books that need to be reviewed every day. They require large number of readers to assess and review books. They are asked to write reviews of about 350 words for each book.

Kirkus Reviews pays an incredible amount and in another words is a typical freelance job. It is a tough competition to get hired for Kirkus, you need to submit few writing samples, and resume that showcases your specialties in reviewing or some other talents that you possess. Usually, copy editors and proofreaders are hired by Kirkus Reviews.

| Kirkus Reviews Payrate: | $50-$75 |

| Apply: | Visit Here |

2. Online Book Club:

Here is another credible website that pays readers for an honest review. It is completely free to be a member of online book club. But before you start earning for reading books on this platform, you need to submit one free review for a book. It serves as an interview to verify your expertise before you can be considered a member of the Online Book Club. Books might be send to you free of cost or you get an e-book to read.

| Online Book Club Payrate: | $5-$60 |

| Apply: | Visit Here |

3. Publishers Weekly:

Publishers’ weekly is a weekly news magazine that primarily focuses on publishing industry. They hire various positions such as qualified proofreaders, copy editors, and book reviewers. Being a book reader, you can choose from proofreaders to being a reviewer. Proofreading is simple, you just need to read manuscripts and mark out some misspellings or grammatical mistakes.

The company seems to publish reviews for all types of books. But to be eligible as a reviewer or to be a proofreader, you need to submit a 200-word review of your own and your recent resume. And you are good to go. Please submit your resumes to reviewers@publishersweekly.com.

| Publishers Weekly Payrate: | $60-$80 |

| Apply: | Visit Here |

4. The US Review of the Books:

It is an online based company that reviews numerous books also pays you for reading. You can earn hundreds of thousands by reviewing books weekly. You get paid on a monthly basis. The pay depends on the length of the book. Reviewers are asked to write a 200 – 300 words book reviews. You have to request reviewer status for this company when they post available books for review on their site.

This website aims to supply honest and objective book reviews to readers. They are looking particularly for informed opinions and professionalism in reviews, along with succinctness. If you want to apply, submit resume, sample work, and two professional references via email at editor@theusreview.com.

| The US Review Payrate: | $25-$75 |

| Apply: | Visit Here |

5. Reedsy Discovery:

Reedsy Discovery is the powerhouse in the world of indie books. It offers reviews a chance to read the latest self-published books before anyone else. You can explore hundreds of new books before choosing one that grabs your attention.

In addition, if you’ve developed your reputation as a book reviewer through Reedsy Discovery, you can communicate with authors who reach out to you directly for a book review. The procedure to apply is pretty simple. To accomplish this, the site offers a form that reviewers must complete. Just complete this form and wait to be selected.

Once you are into them as a book reviewer, you can start looking through shelves and keep reviewing. Book reviewers gets topped for their reviews as a token of appreciation, which is $1, $2 or $5. You even get the free copies of books before they are launched into the market.

| Reedsy Discovery Payrate: | $1-$5 |

| Apply: | Visit Here |

6. BookBrowse:

BookBrowse is another legit company that pays for honest reviews on books. This company aims to help readers pick out the best books for them by publishing book reviews. The website typically aims to hire enthusiastic readers who can also write enthralling reviews of every book they have read on the website.

Unlike other websites, BookBrowse offer the books for free in exchange for reviews you submit. If you’re interested in how, you can become a reviewer for Book Browse, you’ll need to complete out an online form and then send two book reviews samples.

| Apply: | Visit Here |

7. Women’s Review of Books:

Women’s Review of Books specifically aims at women. The website was inspired and developed by the Wellesley Centers for Women at Wesley College. Women’s Review of books has been going on for three decades, examining an array of literary works that include memoirs, poetry, and fiction in addition to other genres.

To enroll into the programme, you need to sign up first, submit a few samples of already published book reviews written by you. You may also be required to tender your resume.

| Women’s Review of Books: | $100 |

| Apply: | Visit Here |

8. Upwork:

Upwork is a platform for various freelancers looking for different types of jobs. This site also includes book reviewers or proofreading. There are a lot of clients (authors) seeking professionals to proofread and check the content of their books. You can earn a good amount of money by reading or editing other people’s blogs, books, articles, posts, or even essays.

First off, you’ll have to join Upwork as a freelancer. Joining Upwork is not expensive, but the platform will take a percentage of the earnings. However, it’s a freelancing platform that lets you bargain with clients and be paid as you wish. If you write a review for $300, it will charge the sum of $60 (which is a 20% of commission).

| Upwork Discovery Payrate: | $18–$35 (per hour) |

| Apply: | Visit Here |

9. eBook Fairs:

Explore the exciting Paid Reader Program on eBook Fairs! Not only do you have the chance to indulge in captivating reads, but you can also earn a bit of extra cash by sharing your thoughtful insights through writing editorial reviews for the books.

Kindly note that your initial two reads and the subsequent editorial reviews, following your application and official acceptance, will be unpaid. This policy applies irrespective of any prior reviews you might have undertaken. Reviews for books with less than 100 pages are free, but if the book is over 100 pages, there’s a fee of $10, unless we’ve mentioned a different amount.

| Upwork Discovery Payrate: | $10 |

| Apply: | Visit Here |

Money

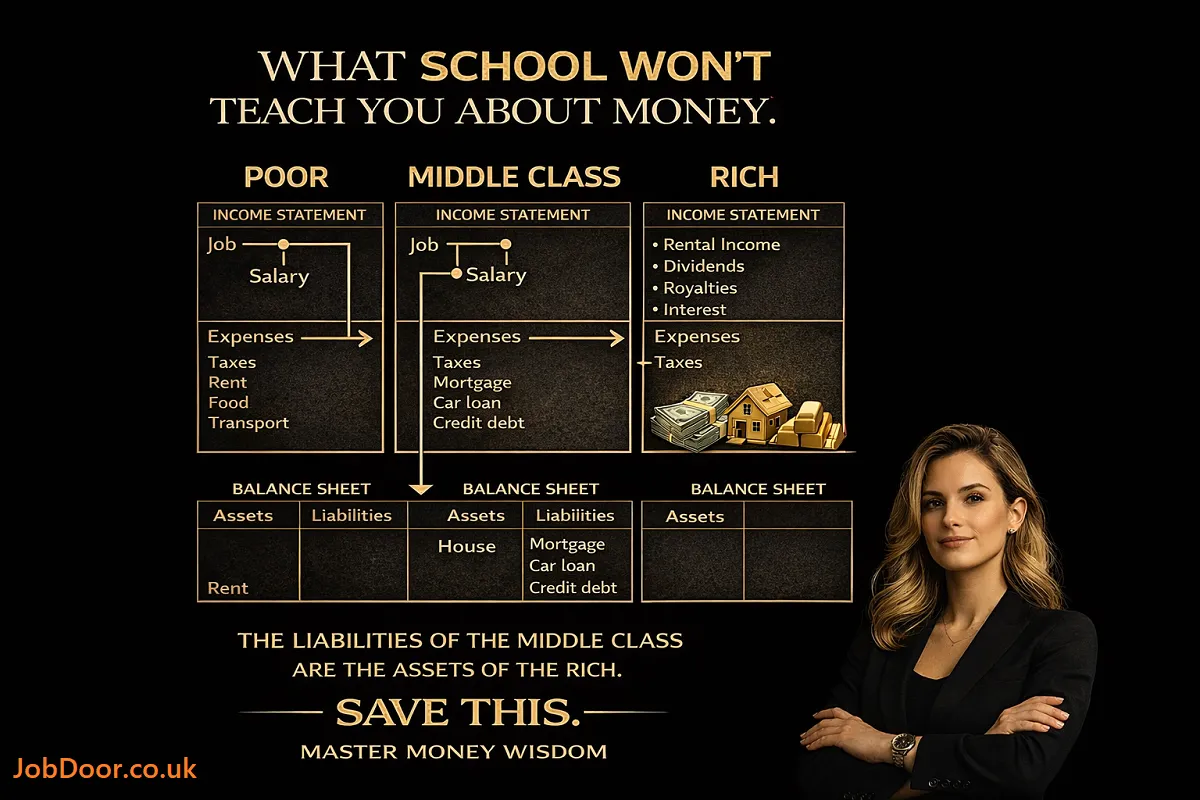

What School Won’t Teach You About Money: The Real Difference Between Poor, Middle Class, and Rich

Most of us spend 12–16 years in school learning mathematics, science, and history. Yet very few of us are taught how money actually works in the real world.

The image above highlights a powerful idea: the financial habits of the poor, middle class, and rich are fundamentally different—especially in how they earn income, manage expenses, and build assets.

If you’ve ever wondered why some people stay stuck financially while others build wealth over time, this guide will break it down in simple, practical terms.

The Core Idea: Income Statement vs Balance Sheet:

Before we compare financial classes, we need to understand two basic concepts:

- Income Statement – Shows how money flows in and out (income vs expenses).

- Balance Sheet – Shows what you own (assets) and what you owe (liabilities).

We are trained to focus on income.

The wealthy focus on assets.

That’s the difference.

1. The Poor: Living on Earned Income Alone

Income Source:

- Job

- Salary

Expenses:

- Taxes

- Rent

- Food

- Transport

- Clothes

- Daily living costs

Balance Sheet:

- Little to no assets

- No significant investments

For many low-income individuals, money flows in and flows out immediately. The paycheck arrives, and it is used to survive. There is no margin to invest or save.

This isn’t about intelligence. It’s about structure.

If your income barely covers essentials, wealth-building becomes extremely difficult. The system forces a cycle:

Work → Get Paid → Spend → Repeat

There is no asset accumulation.

2. The Middle Class: Higher Income, Higher Liabilities

The middle class often earns more than the poor, but their financial structure still limits wealth growth.

Income Source:

- Job

- Salary

Expenses:

- Taxes

- Mortgage

- Car loan

- Credit card debt

- Insurance

- Lifestyle upgrades

Balance Sheet:

- Some assets (home, car)

- Many liabilities (loans, debt payments)

Here’s the critical mistake:

Many middle-class individuals believe their home and car are assets.

In reality:

- If it takes money out of your pocket every month, it is a liability.

- If it puts money into your pocket, it is an asset.

A house with a mortgage is often a liability because:

- It requires EMI payments.

- It generates no monthly income.

- It costs maintenance, taxes, and insurance.

The middle class upgrades lifestyle as income increases:

- Bigger house

- Newer car

- Better gadgets

- More subscriptions

Income rises—but so do expenses.

This creates the “golden cage”:

- High salary

- No financial freedom

3. The Rich: Income from Assets

The wealthy structure their finances differently.

Income Sources:

- Rental income

- Dividends

- Royalties

- Interest

- Businesses

- Investments

Expenses:

- Taxes

- Controlled lifestyle spending

Balance Sheet:

- Income-producing assets

- Few personal liabilities

The wealthy focus on one principle:

Buy assets that generate income.

Instead of working for money, they make money work for them.

Examples of income-producing assets:

- Rental properties

- Dividend-paying stocks

- Businesses

- Digital products

- Royalties from books or music

- Intellectual property

- Bonds

- Private equity

Their financial cycle looks like this:

Asset → Generates Income → Reinvest → Buy More Assets → Repeat

This is compounding at work.

The Powerful Statement:

“The liabilities of the middle class are the assets of the rich.”

This line explains the entire system.

When the middle class:

- Takes a mortgage

- Pays car loans

- Uses credit cards

- Pays rent

Who receives that money?

The asset owner.

For example:

- Your rent = landlord’s rental income

- Your EMI interest = bank’s profit

- Your credit card interest = financial institution revenue

The rich position themselves on the receiving side of cash flow.

Why Schools Don’t Teach This?

Traditional education prepares you to:

- Get good grades

- Get a job

- Earn a salary

It does not teach:

- Cash flow management

- Asset building

- Tax optimization

- Investing

- Entrepreneurship

- Financial psychology

Why?

Because the system was designed during the industrial era to create skilled employees—not investors.

Financial education is usually self-taught.

The Real Difference Is Mindset:

The gap between poor, middle class, and rich is not only income—it’s mindset.

Poor Mindset:

“I need a higher salary to survive.”

Middle-Class Mindset:

“I need a higher salary to afford a better life.”

Wealth Mindset:

“I need assets that generate income so I don’t depend on salary.”

This shift changes everything.

How to Start Moving Toward Wealth?

You don’t need to be rich to begin building assets.

Here’s a practical roadmap.

Step 1: Track Your Cash Flow

Know:

- How much you earn

- How much you spend

- Where your money goes

Awareness is power.

Step 2: Reduce High-Interest Debt

Credit card interest destroys wealth.

Focus on:

- Paying off high-interest loans

- Avoiding unnecessary EMI purchases

Debt reduces your ability to invest.

Step 3: Start Buying Small Assets

You don’t need real estate immediately.

Begin with:

- Index funds

- SIPs

- Dividend stocks

- Digital skills that can create side income

- Freelance services

- Online businesses

Small investments compound over time.

Step 4: Build Multiple Income Streams

Relying on one salary is risky.

Consider:

- Freelancing

- Consulting

- Blogging

- YouTube

- Investing

- Rental opportunities

- Skill-based side gigs

The goal is:

Income that doesn’t require your daily presence.

Step 5: Reinvest, Don’t Inflate Lifestyle

When income increases:

- Don’t immediately upgrade lifestyle

- Upgrade assets first

Wealth grows quietly.

The Psychological Barrier:

Many people remain middle class because they chase comfort over freedom.

- Bigger house feels successful

- Expensive car feels powerful

- Branded lifestyle feels rewarding

But financial freedom comes from:

- Ownership

- Cash flow

- Investment discipline

Delayed gratification separates wealth builders from consumers.

The Truth About Financial Freedom:

Financial freedom doesn’t mean luxury.

It means:

- Your assets pay your expenses.

- You don’t depend entirely on salary.

- You can choose how to spend your time.

The rich focus on:

Time freedom, not status symbols.

Final Takeaway:

The biggest lesson from this image is simple:

- Poor people work for money.

- Middle-class people earn more but increase liabilities.

- Rich people build assets that generate income.

If you remember only one thing, remember this:

Focus on building assets before upgrading lifestyle.

Money is not about how much you earn.

It’s about:

- How much you keep.

- How you invest it.

- Whether it works for you.

Save This Principle:

Be a student of the financial system.

Learn:

- How cash flow works

- How assets grow

- How debt traps people

- How investments compound

Schools may not teach you this—but you can teach yourself.

And once you understand the difference between income and assets, you will never see money the same way again.

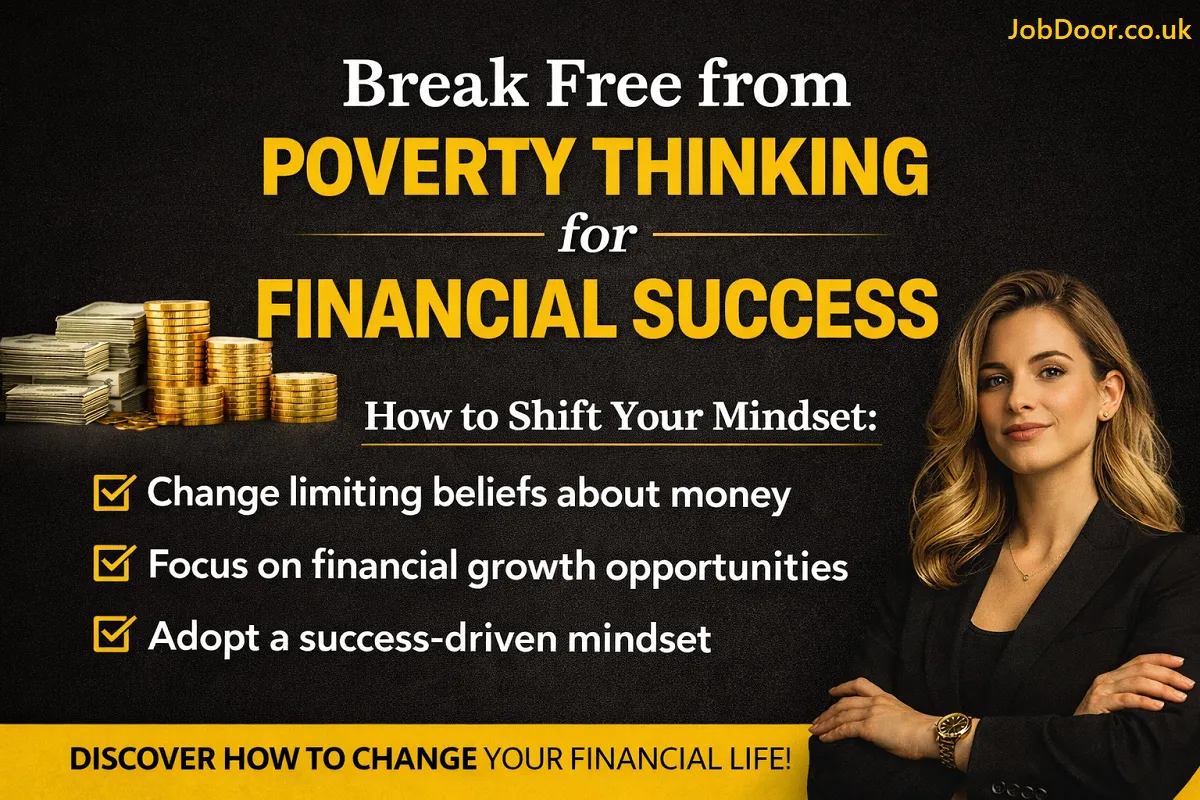

Many people work hard their entire lives yet struggle financially. The problem is not always income — often, it is mindset. A poverty mindset silently shapes decisions, limits opportunities, and keeps people trapped in survival mode instead of growth mode.

Shifting your thinking can be the turning point between financial stress and financial stability. When you begin to see money as a tool for growth rather than something scarce and stressful, your habits, opportunities, and results begin to change.

This guide explains how to break free from poverty thinking, adopt a wealth-building mindset, and create sustainable financial success.

What Is a Poverty Mindset?

A poverty mindset is a pattern of beliefs rooted in fear, scarcity, and limitation. It causes individuals to focus on short-term survival instead of long-term growth.

Common signs include:

- Constant fear of running out of money

- Avoiding investments due to risk anxiety

- Believing wealth is only for “lucky” people

- Living paycheck to paycheck without a plan

- Prioritizing consumption over asset building

This mindset is often shaped by upbringing, environment, financial struggles, and lack of financial education.

The good news is that mindset is learned — and anything learned can be unlearned and replaced.

Why Mindset Matters More Than Income?

Many high earners still struggle financially, while some moderate earners steadily build wealth. The difference lies in habits and thinking.

Your mindset influences:

- Spending behavior

- Risk tolerance

- Investment decisions

- Career growth choices

- Long-term financial planning

A growth-oriented financial mindset focuses on opportunities, skill development, and asset creation rather than immediate gratification.

Step 1: Challenge Limiting Money Beliefs

The first step toward financial success is identifying the beliefs holding you back.

Ask yourself:

- Do I believe money is hard to earn?

- Do I feel guilty wanting financial success?

- Do I think rich people are unethical?

- Do I fear losing money more than I value gaining it?

These beliefs create internal resistance that blocks financial progress.

How to replace limiting beliefs?

- Replace “I can’t afford it” with “How can I afford it?”

- Focus on learning instead of fearing mistakes

- Surround yourself with growth-oriented individuals

- Study successful people who built wealth ethically

Changing beliefs changes behavior — and behavior drives results.

Step 2: Focus on Financial Education

Traditional education rarely teaches practical money management. As a result, many people enter adulthood without understanding savings, investments, taxes, or asset building.

Financial education empowers you to make confident decisions.

Key areas to learn:

- Budgeting and cash flow management

- Debt management strategies

- Investing fundamentals

- Passive income ideas

- Asset vs liability understanding

Even 20 minutes of daily financial learning can dramatically improve long-term outcomes.

Step 3: Shift From Spending to Building Assets

One of the biggest differences between financially struggling individuals and financially successful ones is how money is used.

A poverty mindset prioritizes consumption:

- Upgrading lifestyle quickly

- Buying depreciating items

- Spending to impress others

A wealth mindset prioritizes asset creation:

- Investing in skills

- Building savings and investments

- Creating multiple income streams

Before making purchases, ask:

Will this increase my future income or reduce my financial stress?

This simple question can transform spending habits.

Step 4: Develop Long-Term Thinking

Short-term thinking keeps people trapped in cycles of financial stress. Long-term thinking builds security and freedom.

Instead of focusing only on monthly survival, begin planning for:

- Emergency funds

- Retirement savings

- Investment growth

- Career advancement

- Skill monetization

Small consistent actions over time create powerful financial momentum.

Step 5: Embrace Growth Opportunities

A poverty mindset avoids risk entirely, while a wealth mindset manages risk intelligently.

Growth opportunities may include:

- Learning new high-income skills

- Starting a side business

- Investing gradually

- Networking with growth-oriented individuals

- Taking calculated career risks

Progress rarely happens inside comfort zones.

The goal is not reckless risk — but informed, strategic growth.

Step 6: Build Confidence Around Money

Financial confidence grows through action and knowledge.

Start small:

- Track expenses for awareness

- Save consistently, even if amounts are small

- Learn one investment concept weekly

- Set achievable financial goals

Confidence reduces fear, and reduced fear improves decision-making.

Step 7: Surround Yourself With the Right Environment

Your environment strongly influences your mindset.

If surrounded by negativity, scarcity thinking, or fear of success, growth becomes harder.

Instead:

- Follow educational financial content

- Connect with growth-focused communities

- Read books on money psychology

- Limit exposure to comparison-driven social media

Your mental environment shapes your financial behavior.

Daily Habits That Strengthen a Wealth Mindset:

Consistent habits create lasting change.

Try incorporating:

- Daily financial learning

- Weekly budget reviews

- Monthly goal tracking

- Income diversification planning

- Gratitude for current progress

Small daily improvements create significant long-term transformation.

The Emotional Side of Financial Growth:

Breaking poverty thinking is not just about money — it is emotional.

It involves:

- Letting go of fear

- Healing financial stress patterns

- Building patience and discipline

- Learning delayed gratification

Financial success is as much psychological as it is practical.

Final Thoughts: Financial Freedom Starts in the Mind

Your financial future is not determined solely by income, background, or circumstances. It is heavily influenced by beliefs, habits, and decisions.

When you shift from scarcity to growth thinking:

- Opportunities become visible

- Confidence increases

- Smart risks feel manageable

- Long-term planning becomes natural

- Wealth building becomes achievable

Financial success is not an overnight transformation — it is a gradual process of mindset, learning, and consistent action.

The most powerful investment you can make is in your thinking.

Money rarely disappears overnight. More often, it slips away quietly through small habits, unnoticed expenses, and lifestyle patterns that feel harmless in the moment. You may earn a decent income, avoid major debt, and still wonder why saving feels difficult.

This silent drain is not about poor financial discipline — it’s usually about unseen spending behavior. Once you recognize these hidden money leaks, you can regain control without sacrificing your quality of life.

This guide explores the most common ways money disappears without you noticing and provides practical strategies to fix each one.

1. The Upgrade Trap

Modern marketing constantly encourages upgrades — better phones, premium subscriptions, faster plans, and luxury versions of everyday items. While each upgrade seems small, the cumulative effect can significantly increase monthly expenses.

The problem isn’t upgrading itself. It’s automatic upgrading without evaluating real value.

Why it happens

- Desire for convenience and comfort

- Social comparison

- Emotional satisfaction from “better” products

How to fix it

- Pause before upgrading and ask if the current item still works well

- Delay upgrades for 30 days to test if the desire fades

- Prioritize functional upgrades instead of lifestyle upgrades

Often, keeping something slightly older but functional provides more financial freedom than constant upgrading.

2. Subscription Fog

Streaming services, apps, software tools, memberships, and auto-renewing plans create one of the biggest hidden spending categories today. Individually, they feel inexpensive. Together, they can quietly consume a large portion of your budget.

Many people pay for services they rarely use simply because the payment is automatic.

Why it happens

- Low monthly pricing reduces perceived impact

- Free trials convert into paid plans

- Lack of visibility in monthly spending

How to fix it

- Review bank statements every month specifically for subscriptions

- Cancel anything unused for 30 days or more

- Replace multiple services with one high-value option

A simple subscription audit can instantly free up meaningful savings.

3. Convenience Spending

Convenience often comes with hidden costs — food delivery, ride-sharing, express shipping, pre-packaged meals, and premium service fees. While these options save time, frequent reliance on them increases spending without improving long-term financial stability.

Convenience is valuable, but unconscious convenience becomes expensive.

Why it happens

- Busy schedules

- Habit formation

- Emotional fatigue leading to quick decisions

How to fix it

- Reserve convenience spending for high-stress days only

- Prepare simple backup solutions (easy meals, planned transport)

- Track convenience purchases for one week to build awareness

Even reducing convenience spending slightly can produce noticeable financial improvement.

4. Social Spending Pressure

Keeping up with friends, coworkers, or social circles can lead to spending that doesn’t align with your priorities. Dining out frequently, attending costly events, or participating in group purchases can quietly stretch your budget.

The goal isn’t isolation — it’s intentional participation.

Why it happens

- Fear of missing out

- Desire for belonging

- Unspoken social expectations

How to fix it

- Suggest low-cost alternatives like coffee, walks, or home gatherings

- Set a monthly social budget

- Learn to decline invitations without guilt

Healthy relationships don’t require constant spending.

5. The Small Expense Illusion

Small daily purchases feel harmless — coffee, snacks, impulse online buys, or minor add-ons. Individually they seem insignificant, but repeated frequently, they become powerful budget leaks.

The issue isn’t small spending — it’s untracked small spending.

Why it happens

- Emotional rewards

- Habitual buying

- Lack of spending visibility

How to fix it

- Track small expenses for one week

- Bundle similar purchases into a weekly allowance

- Replace routine impulse buys with planned treats

Awareness alone often reduces unnecessary micro-spending.

6. Lifestyle Anchoring

When income increases, spending often increases alongside it. This creates a cycle where financial progress feels stagnant despite earning more.

This pattern is known as lifestyle anchoring — adjusting expenses upward to match income rather than building savings.

Why it happens

- Desire to reward hard work

- Gradual normalization of higher spending

- Lack of automatic saving systems

How to fix it

- Increase savings before increasing lifestyle expenses

- Set percentage-based saving rules

- Maintain some elements of your previous lifestyle

Financial growth happens when income grows faster than lifestyle.

7. Frictionless Payment Habits

Digital wallets, tap-to-pay systems, and one-click purchases remove the psychological pause that once accompanied spending. The easier it is to pay, the easier it is to overspend.

Convenience in payments can unintentionally reduce spending awareness.

Why it happens

- Instant gratification

- Reduced emotional connection to money

- Minimal spending reflection

How to fix it

- Use manual payment methods for non-essential purchases

- Enable purchase notifications

- Introduce a 24-hour delay for discretionary spending

A small pause before buying can prevent many unnecessary expenses.

8. Hedonic Adaptation

Exciting purchases quickly become normal. The satisfaction fades, but the financial impact remains. This leads to repeated spending in search of the same emotional boost.

Understanding this pattern helps reduce impulse purchases driven by temporary excitement.

Why it happens

- Emotional reward cycles

- Marketing influence

- Short-lived satisfaction

How to fix it

- Focus spending on experiences rather than constant upgrades

- Practice gratitude for existing possessions

- Delay purchases to test lasting value

Long-term satisfaction rarely comes from repeated material spending.

9. Future Self Neglect

Many people prioritize present comfort over future financial security — not intentionally, but subconsciously. Retirement savings, emergency funds, and long-term investments often feel distant compared to immediate desires.

Ignoring future needs allows money to disappear today without visible consequences — until later.

Why it happens

- Difficulty visualizing the future

- Lack of urgency

- Competing short-term priorities

How to fix it

- Automate savings and investments

- Create specific future goals

- Treat savings like a fixed monthly expense

Protecting your future self is one of the most powerful financial decisions you can make.

How to Stop Money From Disappearing

Understanding these habits is only the first step. The real transformation comes from building simple systems that protect your finances automatically.

Practical strategies that work

✅ Track spending weekly instead of monthly

✅ Automate savings immediately after income arrives

✅ Create spending categories instead of strict restrictions

✅ Review subscriptions quarterly

✅ Set guilt-free spending limits for enjoyment

Financial control doesn’t require extreme restriction — it requires awareness and intention.

The Real Secret: Awareness Over Discipline

Many people believe they struggle with money because of weak discipline. In reality, the biggest issue is lack of visibility. When spending becomes visible, behavior naturally improves.

Instead of focusing on strict budgeting, focus on:

- Awareness

- Alignment with priorities

- Conscious decision-making

Small adjustments in awareness can produce major financial improvements over time.

Final Thoughts

Money rarely disappears through one major mistake. It fades through quiet habits, unnoticed subscriptions, emotional spending, and lifestyle patterns that feel normal.

The good news is that these leaks are completely fixable.

You don’t need to eliminate enjoyment, stop socializing, or avoid convenience altogether. You simply need to recognize where your money is going and decide whether it truly adds value to your life.

Once you gain that clarity, saving becomes easier, financial stress decreases, and your money begins working toward your goals instead of disappearing unnoticed.

If you’d like, I can also help you with:

✅ Pinterest titles & descriptions for this topic

✅ SEO meta title + meta description

✅ Featured snippet optimization

✅ Internal linking ideas for your blog

✅ A high-CTR conclusion or CTA section

Just tell me.

6 AI Tools that Can Automate Your Work and Save 1,000+ Hours of Work

Artificial intelligence is no longer a futuristic concept reserved for tech experts. It has become a practical companion for students,...

I Tested 250+ AI Tools — Here Are 15 Hidden Gems Worth Using in 2026

Artificial intelligence is expanding at an incredible pace, with hundreds of new tools launching every month. While most people only...

25 New AI Tools Everyone Will Be Using in 2026 (Most People Don’t Know)

Artificial intelligence continues to evolve at a breathtaking pace, and 2026 has already introduced a wave of innovative AI tools...

AI Basics That Will Save You Hours Every Week (Everybody Must Know)

Artificial Intelligence is no longer a futuristic concept. It’s already shaping how we search online, create content, run businesses, and...

Why AI Is a Wealth-Building Skill in 2026?

Artificial intelligence is no longer a futuristic concept — it’s a practical income tool that everyday creators, freelancers, bloggers, and...

The 7 Best AI Tools for Beginners in 2026 (Start Using AI Today)

Artificial Intelligence is everywhere right now. You hear about it on YouTube, social media, blogs, and even casual conversations. People...

What School Won’t Teach You About Money: The Real Difference Between Poor, Middle Class, and Rich

Most of us spend 12–16 years in school learning mathematics, science, and history. Yet very few of us are taught...

Break Free From Poverty Thinking & Build Real Wealth

Many people work hard their entire lives yet struggle financially. The problem is not always income — often, it is...

9 Ways Money Disappears Without You Noticing (And How to Take Back Control)

Money rarely disappears overnight. More often, it slips away quietly through small habits, unnoticed expenses, and lifestyle patterns that feel...

What to Say When a Colleague Leaves (Perfect Goodbye Email Ideas)

Saying goodbye at work is never easy. One day you’re sharing coffee breaks, deadlines, and inside jokes — and the...

YouTube Automation: Make $10K Monthly Without Even Showing Your Face

What if you could build a profitable YouTube channel… without filming yourself, buying expensive gear, or becoming an on-camera personality?...

My Boss Is Leaving — What to Say: The Perfect Goodbye Email or Message to Your Boss

Your boss is leaving. And suddenly, you’re stuck wondering what to say. Do you keep it formal? Do you express...

10 Places Where Rich People Give Away Free Money (And How You Can Get It)

Let’s be honest. The idea of getting free money sounds too good to be true. Most of us instantly think...

Top 5 AI Trends That Will Define 2026 – It Will Change Everything

Let’s be honest. When people talk about AI and the future, it can feel overwhelming.New tools. New trends. Big predictions....

I Tried 100 AI Tools: These 7 Can Help You Make Money in 2026

Everywhere you look, someone is talking about AI. “AI will replace jobs.”“AI is the fastest way to make money.”“Use this...

AI Business Ideas You Can Start Today (No Tech Skills Needed)

AI is everywhere right now. You hear people say: But instead of feeling excited, you might feel confused, anxious, or...

ChatGPT Prompts to Create Viral YouTube Shorts

YouTube Shorts look simple on the surface. A short video.A few seconds.Quick views. But when you actually sit down to...

5 Underrated Digital Skills You Can Learn at Home That Most People Still Ignore

If you’ve read even a few career blogs, you’ve seen the same advice again and again. Learn content writing.Learn graphic...

25 Best-Selling Digital Products You Can Create Once and Sell Forever

If you’ve ever searched online for ways to make passive income, you’ve probably felt overwhelmed. So many options.So much jargon.So...

5 Powerful Ways to Monetize Your Facebook Group (Even If You’re Starting From Zero)

You started a Facebook group for a reason. Maybe to share knowledge.Maybe to connect people with similar interests.Maybe just for...

-

Career2 years ago

Career2 years agoCareer Opportunities for Seniors: 7 Jobs that are Perfect for Older Adults

-

Money1 month ago

Money1 month ago26 Lucrative Passive Income Ideas to Build Wealth in 2026

-

Job Description2 years ago

Job Description2 years agoGraphic Designer Job Description: Education, Salary, Skills, Work Hours

-

News2 years ago

News2 years agoStudents’ question to UK PM Rishi Sunak: “What if your kids started smoking?

-

Career2 years ago

Career2 years ago13 Best Jobs That AI Can’t Replace: A Guide to Future-proof Careers

-

Career2 years ago

Career2 years agoStandard Employment Contract Template Example for UK (Word & PDF)

-

AI & Tools1 month ago

AI & Tools1 month agoChatGPT vs Copilot: Which AI Is Best for You in 2026?

-

Job Description2 years ago

Job Description2 years agoSupport Worker Job Description: Qualifications, Skills, Salary, Working Hours